On 26 May 2026, the Federal Court of Australia ordered two businesses to pay civil penalties of $50,000 and $45,000, plus costs, after they failed to pay AUSTRAC infringement notices of $18,780 each. No money laundering scheme. No exotic crypto typology. No headline-grabbing scandal. The original failure was about as mundane as AML compliance gets: they did not lodge their annual compliance report on time. For the roughly 90,000 lawyers, accountants, real estate agents, conveyancers and dealers entering the regime on 1 July 2026, this small, unglamorous case is the most instructive enforcement story of the year. (Financial Newswire coverage)

What Actually Happened

The facts are worth following carefully, because the lesson is in the sequence, not the headline number.

In September 2024, AUSTRAC issued infringement notices to 16 businesses for failing to submit their annual compliance report for the 2023 calendar year, a standing obligation under the Anti-Money Laundering and Counter-Terrorism Financing Act. Two of those businesses, Castra Licensee Pty Ltd and Princeton Securities (NSW) Pty Ltd, each received a notice for $18,780.

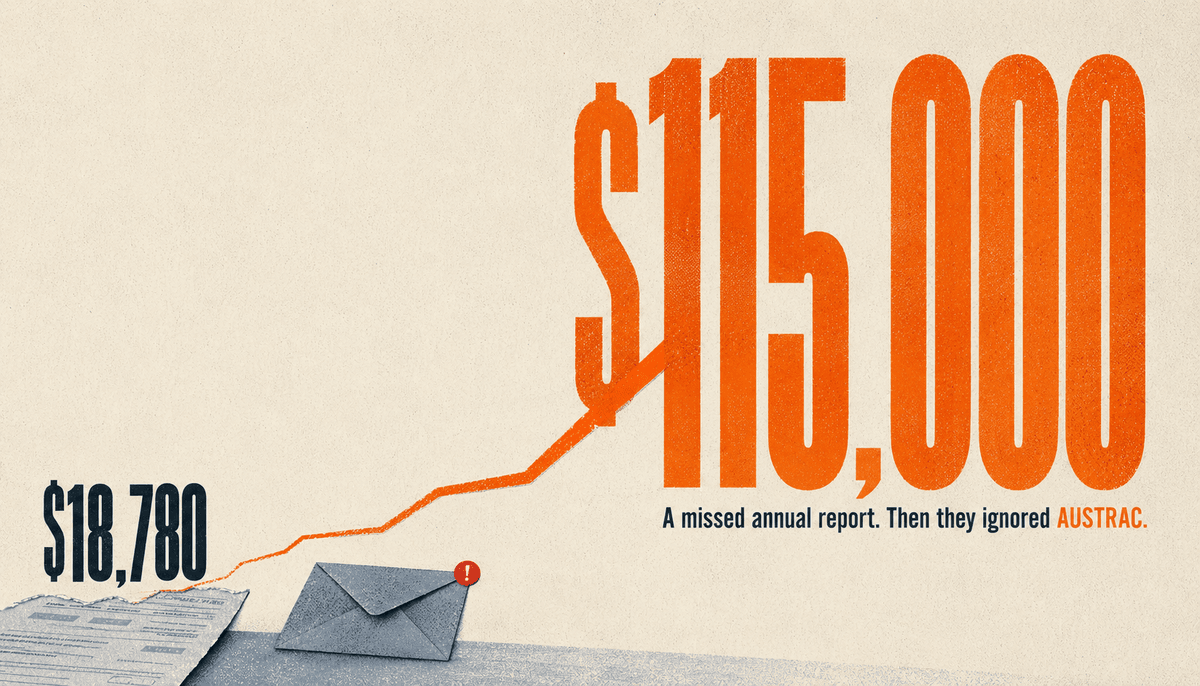

An infringement notice is, in effect, the cheap exit. Pay it, and the matter ends. Neither business paid. So AUSTRAC commenced civil penalty proceedings in the Federal Court, and on 26 May 2026 Justice Lee handed down the orders. Castra was ordered to pay a $50,000 penalty plus $15,000 in costs. Princeton, which admitted liability and made joint submissions with AUSTRAC on penalty, was ordered to pay an agreed $45,000 plus $5,000 in costs. The combined financial impact lands north of $115,000, against original notices of $18,780 each. (AUSTRAC's own account of the outcome via ACAMS)

Read that arithmetic slowly. A single missed administrative report became an $18,780 notice. Ignoring the notice turned $18,780 into roughly $65,000 for Castra all in. The breach did not get worse. The decision to ignore the regulator did.

Why This Is the Tranche 2 Case To Study

It is tempting for a professional firm to dismiss this as a financial-services-licensee problem with nothing to teach an accountant or a conveyancer. That instinct is exactly backwards, for one simple reason.

The annual compliance report is the single most predictable obligation in the entire regime, and from 1 July 2026, Tranche 2 firms will have it too. It is not triggered by a suspicious customer or an unusual transaction. It does not require judgement about source of funds or a fine call about whether to lodge a suspicious matter report. It arrives on a schedule, every year, and the only thing it asks is that you complete and lodge it on time. It is the obligation with the fewest excuses attached. (What the annual compliance report deadline means for Tranche 2)

And it is precisely this obligation that AUSTRAC pursued, against small businesses, all the way to the Federal Court, over a 2023 report. The signal for the 90,000 new entrants is hard to misread. If the regulator will take a missed annual report this far for existing reporting entities who had years of practice with the regime, the idea that newly regulated firms get an informal grace period on the basics does not survive contact with the evidence.

Three Lessons For Every New Reporting Entity

The cheapest moment to deal with AUSTRAC is the first one. An infringement notice is the off-ramp, not the punishment. $18,780 was the price of making the matter disappear. The businesses that ignored it did not avoid the cost, they multiplied it and added Federal Court proceedings, costs orders, and a public enforcement record on top. Whatever a notice from AUSTRAC says, the worst available response is to file it under "deal with later." Engagement is almost always cheaper than avoidance. (How AUSTRAC penalties and enforcement escalate)

Cooperation is not a soft virtue, it is a line item. Look at the gap between the two outcomes. Princeton admitted liability and worked with AUSTRAC on joint submissions about the appropriate penalty, and its costs order was $5,000. Castra's costs order was $15,000, three times as much. The Court explicitly factored each business's level of cooperation into the result. For a small firm, that is a concrete, money-on-the-table reason to engage constructively the moment AUSTRAC makes contact, rather than going quiet and hoping it passes.

A routine obligation missed is still a breach, and AUSTRAC treats it as one. There is a comfortable assumption in professional services that the regulator only cares about the dramatic stuff: the laundered millions, the deliberate concealment, the sophisticated structuring. This case is the counterexample. The breach here was a piece of annual paperwork that did not get filed. AUSTRAC pursued it anyway, because a reporting regime that does not enforce its most basic, most predictable obligation is not a regime at all. The unglamorous obligations are not the safe ones to skip. They are the ones with no defence when skipped. (How SMR and TTR reporting fit alongside the annual report)

What To Put In Place Before 1 July

The defence against ending up in a story like this one is almost embarrassingly simple, which is exactly why missing it is so costly. Three things deserve a place in your firm's calendar and your program before obligations begin.

First, know your reporting obligations and when they fall. The annual compliance report is the headline, but it sits alongside threshold transaction reports and suspicious matter reports. A firm that has written down what it must report, and when, does not miss a deadline by accident. (What an AML/CTF program covers, Part A to F)

Second, give the calendar an owner. A deadline that belongs to "the firm" belongs to no one. Your named AML/CTF compliance officer should own the reporting calendar, with a reminder system that does not depend on someone happening to remember in the right week. The whole Castra and Princeton saga started with a single report that nobody lodged.

Third, never ignore a letter from AUSTRAC. If a notice, a request, or an audit instrument arrives, the response is to engage promptly, get advice if you need it, and deal with it while it is still cheap. The two businesses in this case had the option to end the matter for $18,780 and chose silence instead. Silence is the single most expensive choice in this entire story.

The One Sentence To Take Away

The breach was small. The bill was not, because the firms ignored AUSTRAC. From 1 July 2026 your firm will carry the same annual compliance obligation these two businesses missed, and the same regulator that took a $18,780 report all the way to the Federal Court will be watching whether you lodge it. The obligation is predictable, the deadline is known, and the cost of getting it wrong now has a public number attached: more than $115,000.

Where AML Mate Fits

AML Mate builds the parts that keep a routine obligation from becoming a Federal Court matter: a Part A to F program mapped to your designated services, a named compliance officer structure, and a clear view of the reporting obligations your firm carries so the annual compliance report is a diarised task, not a forgotten one. The free compliance check at /check gives you a five-minute read on whether your firm is set up to meet its reporting obligations before 1 July 2026. Five minutes now is considerably cheaper than $65,000 later.