"Where did the money come from?" sounds like a single question. Under the AML/CTF Act, it is actually two — and most reporting entities conflate them. AUSTRAC auditors do not. Getting these wrong is one of the most common causes of enhanced due diligence (EDD) failing a review.

This guide sets out the difference, what AUSTRAC expects you to document, and how to do it without turning every high-risk onboarding into a three-week investigation.

The Core Difference

| Source of Funds (SOF) | Source of Wealth (SOW) | |

|---|---|---|

| What it asks | Where did the money for this transaction come from? | How has this customer accumulated their wealth overall? |

| Scope | Transactional, narrow | Biographical, broad |

| Timeframe | The specific transaction | Years or decades of income |

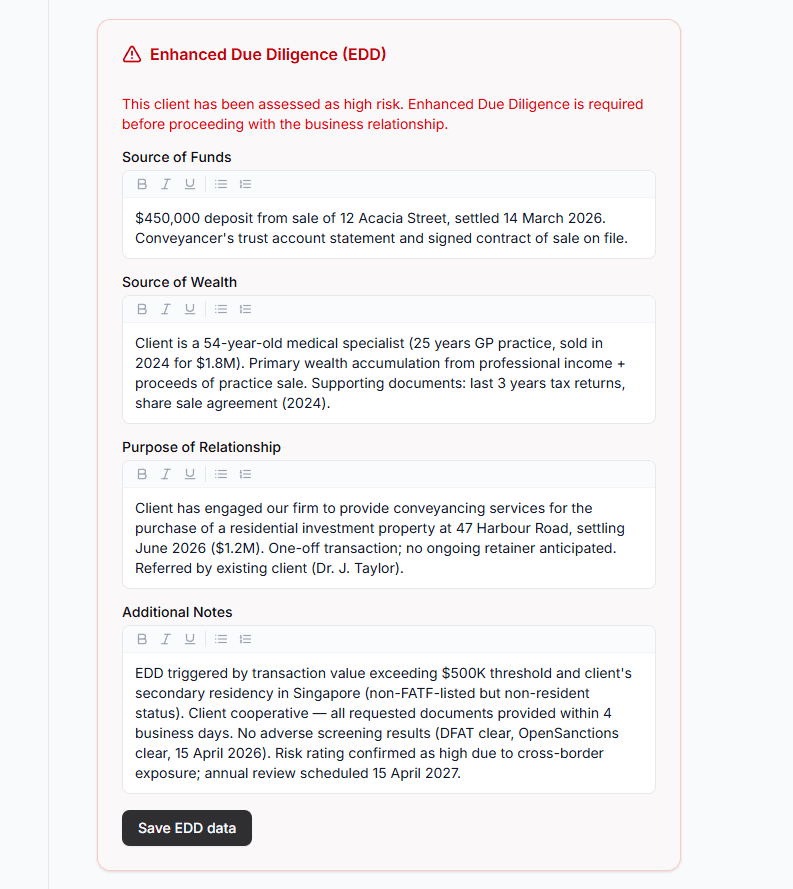

| Example | "$450,000 deposit came from sale of 12 Acacia Street on 14 March 2026" | "Mr Smith's net worth is from 20 years as a medical specialist plus inherited property" |

| When required | Most customer relationships, especially when transactions look unusual for the customer's profile | Enhanced Due Diligence — high-risk customers, PEPs, complex structures |

If you ask only SOF on a high-risk client, you have done half the job. A legitimate-looking SOF (a bank transfer from an offshore account) can still conceal illegitimate SOW (how did they get the offshore account in the first place).

What AUSTRAC Wants to See — With Examples

Documenting Source of Funds

Acceptable SOF documentation includes any of the following that match the transaction amount and date:

- Sale proceeds — contract of sale, settlement statement, conveyancer's trust account statement

- Employment income — recent payslips, PAYG summary, employment contract

- Business income — BAS statements, company financials, accountant's letter

- Loan — loan contract from a regulated Australian lender

- Inheritance — grant of probate, executor's distribution statement

- Savings — bank statements showing the accumulation period, not just the current balance

- Investment liquidation — broker statement showing sale of shares or units

The test: can the customer produce a paper trail from the transaction back to a legitimate origin, and do the amounts reconcile?

Documenting Source of Wealth

SOW is harder because it is cumulative. You are not tracing one transaction — you are building a plausible picture of the customer's economic history. Acceptable evidence includes:

- Career history + income — LinkedIn or CV plus 2–3 years of tax returns or payslips

- Business ownership — ASIC extract showing directorship history, company financials over time

- Inheritance — grant of probate, deceased estate documentation

- Sale of major assets — sale contract for a business, property, or investment portfolio

- Long-term investment returns — portfolio statements showing growth over years

- Professional valuation — for complex wealth (private business, art, intellectual property)

The test: does the customer's lifestyle and asset base reconcile with the income history they have described? If a 35-year-old paralegal presents $5 million in liquid assets, "savings from salary" does not reconcile.

When Do You Actually Need Both?

You do not need to document SOW on every customer. The AML/CTF Rules require SOW only when enhanced due diligence (EDD) is triggered. That typically means:

- The customer is a politically exposed person (PEP), their family member, or close associate

- The customer is from, or transacting with, a high-risk jurisdiction (FATF grey/black list, DFAT sanctioned countries)

- The customer presents high residual risk after your initial risk assessment

- You have suspicions about the customer's profile that are not strong enough to be an SMR but cannot be dismissed

- A transaction is significantly inconsistent with what you know about the customer

For everyone else, documenting SOF on unusual or high-value transactions is usually sufficient.

A 10-Minute Process for High-Risk Clients

Do not turn this into a research project. For a typical EDD case:

Step 1 — Ask in plain English (3 min). "For this transaction, can you tell me where the funds came from?" and "More broadly, can you give me a picture of how you've built up your assets over the years?" Record what they say verbatim.

Step 2 — Match words to documents (4 min). For each claim, note what evidence would substantiate it. Sale of a property → sale contract. 20 years as a consultant → last 2 years of tax returns. Company sale → completed share sale agreement.

Step 3 — Collect the evidence (variable, often async). Ask the client to provide the documents. Give them 7–14 days.

Step 4 — Reconcile (3 min). Do the amounts and dates line up? Does SOW explain the scale of SOF? Any gaps? Any red flags (large unexplained deposits, jurisdictions not mentioned in the interview, dates that do not match)?

Step 5 — Record your conclusion (1 min). Write a short file note stating what you asked, what they answered, what documents you reviewed, and whether you are satisfied. This file note is the single most important document if AUSTRAC ever asks.

Three Mistakes That Fail EDD Reviews

Using "source of funds" as a synonym for "source of wealth." If your EDD file contains only bank statements for the specific transaction on a PEP client, your SOW is missing. AUSTRAC auditors check for this pattern specifically.

Accepting the customer's word without documentation. A verbal explanation is a start, not a conclusion. The file must contain independent evidence. "Client advised funds came from business sale" without a copy of the share sale agreement is a documented gap, not a completed EDD.

Stopping at the first layer. If SOF shows a transfer from Customer A's personal bank account, that is not the source of funds — that is an intermediate step. Where did Customer A's bank account get the money? The audit trail needs to reach a legitimate economic origin (salary, sale, inheritance, loan), not just another of the customer's own accounts.

How AML Mate Handles This

EDD is one of the highest-friction moments in client onboarding. AML Mate's client record includes dedicated SOF and SOW fields, document upload slots with labelled categories (sale contract, tax return, probate, etc.), and AI-assisted drafting of the file note that reconciles your questions, their answers, and the documents collected — so your EDD record is audit-ready the day you close it, not six months later when someone asks.

With 71 days until 1 July 2026, your EDD process is one of the last things to lock in. Get the SOF / SOW distinction right now, and the rest of enhanced due diligence follows.

Related reading: